The best credit card for travel to Ireland (2024) is the perfect way to improve your trip experience. Holding the best financial tool in your toolbox can be extremely helpful as you set out on your journey to reach the Golden Island. We are going to look at the best credit card choices designed especially for travel to Ireland in 2024. We can help you with everything from maximizing rewards to lowering expenses. Let’s get started and make sure you have the most amazing trip to Ireland possible.

The Ultimate Guide to Finding the Best Credit Card for Ireland Travel

Introduction

Planning a trip to Ireland involves extreme care and attention to detail, from selecting accommodations to making travel arrangements. Choosing the best credit card is one of these factors that can greatly improve your trip. All the information you require to select the best credit card for travel to Ireland will be covered in this detailed guide.

Understanding the Importance of the Best Credit Card for Ireland Travel

Going off for Ireland offers plenty of chances for discovery and excitement. Without the best funds, dealing with international transactions, currency exchange rates, and travel benefits can be difficult. This section explores the reasons why a smooth and satisfying trip to Ireland requires the best credit card.

- Ireland’s Diverse Landscapes and Rich Cultural Heritage: The country is home to an abundance of historical sites, from fertile farmland to old castles.

- Having the best credit card guarantees that you may enjoy the country’s services without worrying about financial issues.

Convenience and Security: You may take advantage of increased security features like fraud protection and travel insurance, as well as the convenience of cashless purchases, when you use the best credit card for traveling to Ireland.

Increasing Travel Benefits and Rewards: By choosing the best credit card, you may take advantage of travel benefits like hotel stays, airline miles, and cashback incentives, which will increase the overall worth of your trip to Ireland.

Best Credit Card for Ireland Travel: Top Recommendations

After thorough research and consideration of the aforementioned factors, here are our top recommendations for the best credit cards for Ireland travel:

1. Chase Sapphire Preferred® Card

- Reward: Receive extra points for dining and travel-related purchases.

- No fees apply to foreign transactions.

- Full protection is provided by travel insurance.

- acceptance: generally recognized on a global scale.

- Annual Charge: $95.

2. Capital One Venture Rewards Credit Card

- Reward: Collect unlimited miles with each transaction.

- No fees apply to foreign transactions.

- Travel Insurance: Different kinds of protections are available.

- Acceptance: Accepted everywhere with no fees for international transactions.

- Annual Charge: $95.

3. American Express® Gold Card

- Reward: Collect Membership Rewards points when dining and traveling.

- No fees apply to foreign transactions.

- Limited coverage is offered by travel insurance.

- acceptance: Generally recognized particularly in large cities.

- $250 as an annual fee.

Factors to Consider When Choosing the Best Credit Card for Ireland Travel

1. Awards Program

Research credit cards designed for visitors that offer generous rewards. Look out credit cards that give extra points or miles for travel-related costs like meals, hotels, and airfare.

2. Fees for International Transactions

Choose a credit card that does not apply international transaction fees to save money on unnecessary expenses when shopping overseas. These costs may build quickly and reduce the value of your travel budget.

3. Coverage for Travel Insurance

Give top priority to credit cards that provide full travel insurance, such as emergency medical help, reward for lost luggage, and trip cancellation/interruption insurance.

4. Accessibility and Acceptance

Make sure your credit card can be used to easily withdraw cash from an international network of ATMs and is generally accepted in Ireland.

5. The Chip-and-PIN Method

Check to see if your credit card has chip-and-PIN technology, which is widely used in Europe to provide extra protection when making purchases.

6. Customer Service and Help

Choose a credit card provider with an outstanding track record for helping customers, particularly in case of emergencies or unexpected situations when traveling.

7. Annual Charges

Analyze the total value proposition by evaluating the annual costs related to each credit card and comparing them to the possible incentives and advantages provided.

8. First-Time Offers

To get the most out of your credit card, take advantage of introductory offers like sign-up bonuses, 0% APR periods, and reduced annual fees.

FAQs

Which credit card is best for travel to Ireland?

- The best credit card for traveling to Ireland will rely on personal tastes and spending patterns. However, the American Express® Gold Card, Capital One Venture Rewards Credit Card, and Chase Sapphire Preferred® Card are well-liked options.

Do credit cards come with an option for avoiding foreign transaction fees?

- Yes, a few credit cards have no foreign transaction fees, which makes them perfect for trips abroad. The Discover It® Miles program, Capital One Venture Rewards Credit Card, and Chase Sapphire Preferred® Card are a few examples.

What features should a credit card for traveling to Ireland offer?

- Consider characteristics like worldwide acceptance, no foreign transaction fees, comprehensive travel insurance coverage, and rewards programs customized for travel costs when selecting a credit card for your trip to Ireland.

How can I use a credit card in Ireland without having to pay currency conversion fees?

- Choose a credit card with no international transaction fees if you want to avoid paying currency exchange fees when using it in Ireland.

I want to travel to Ireland; can I use my debit card for expenses?

- Debit cards can be used in Ireland for travel spending, but they do not provide the same protections and benefits as credit cards, like reward programs and travel insurance.

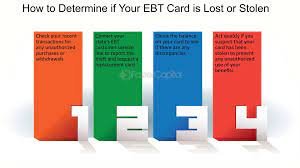

When staying in Ireland, what should I do if my credit card is lost or stolen?

- Get in touch with your card issuer right away to report the occurrence and ask for a new card if your credit card is lost or stolen while you are staying in Ireland.

Conclusion

In Conclusion, Choosing the best credit card for travel to Ireland is important to a smooth and rewarding trip, not just from a financial standpoint. Travelers can make well-informed decisions that improve their overall experience by carefully considering aspects including rewards programs, international transaction costs, travel insurance coverage, and card acceptance.

You can be sure that you have the financial tools to take full advantage of your trip through the Sapphire Island, no matter whether you choose to take advantage of the adaptable benefits of the Chase Sapphire Preferred® Card, the unlimited miles of the Capital One Venture Rewards Credit Card, or the special benefits of the American Express® Gold Card. You may travel around Ireland’s amazing landscapes, take in its unique culture, and make lasting impressions with peace of mind if you have the correct credit card.